When Sarah, a public school teacher in the United States, started planning her retirement, she heard two common terms from her HR department: 403b and IRA.

She wondered about the difference between 403b and IRA and which one would secure her future better. Like Sarah, many employees struggle to understand the difference between 403b and IRA because both are retirement savings plans.

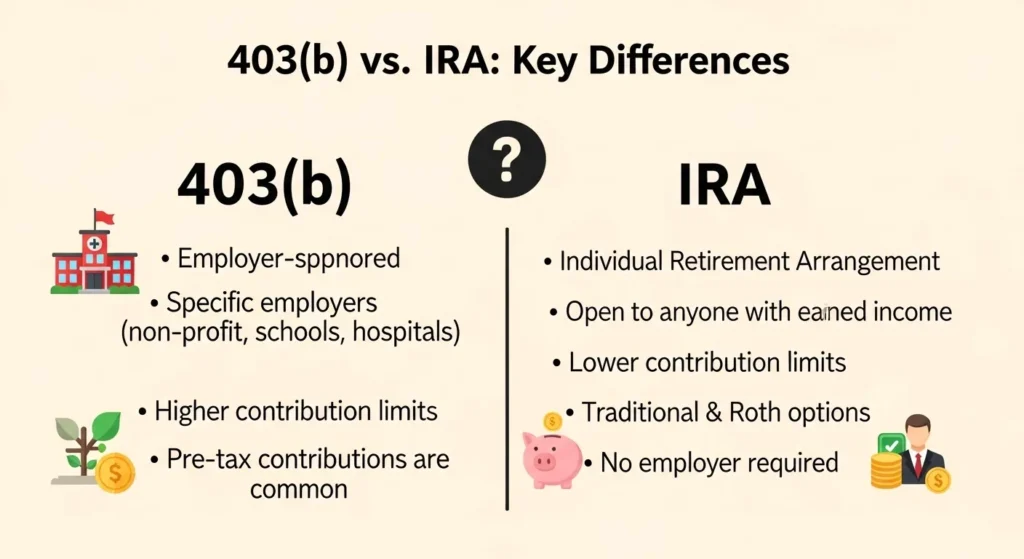

A 403b is an employer-sponsored retirement plan mainly for public school employees and nonprofit workers. An IRA (Individual Retirement Account) is a personal retirement savings account that anyone with earned income can open.

Understanding the difference between 403b and IRA helps individuals choose wisely. In fact, the difference between 403b and IRA can significantly affect long-term savings, taxes, and financial security.

Before we dive deeper, let’s first clarify how these terms are pronounced and then explore the detailed comparison.

Pronunciation (US & UK)

- 403b

- US: /ˌfɔːr ˌθriː ˈbiː/

- UK: /ˌfɔː ˌθriː ˈbiː/

- US: /ˌfɔːr ˌθriː ˈbiː/

- IRA

- US: /ˌaɪ ɑːr ˈeɪ/

- UK: /ˌaɪ ɑːr ˈeɪ/

- US: /ˌaɪ ɑːr ˈeɪ/

Now that we understand the basics, let’s move to the core discussion.

Key Difference Between the Both

The main difference between 403b and IRA lies in eligibility and contribution structure. A 403b is offered through an employer (mainly nonprofits and public institutions), while an IRA is opened individually without employer involvement.

Why Is Their Difference Necessary to Know for Learners and Experts?

Understanding the difference between 403b and IRA is important because retirement planning affects economic stability in society.

- For learners: It builds financial literacy early in life.

- For experts: It helps in advising clients accurately.

- For society: Better retirement planning reduces dependence on social welfare systems and strengthens financial independence.

Difference Between 403b and IRA

1. Eligibility

403b: Only for employees of public schools and nonprofit organizations.

- Example 1: A public school teacher can join a 403b.

- Example 2: A hospital nurse in a nonprofit hospital qualifies.

IRA: Anyone with earned income can open it.

- Example 1: A freelancer can open an IRA.

- Example 2: A self-employed consultant can invest in an IRA.

2. Employer Involvement

403b: Sponsored by employer.

- Example 1: Employer deducts contributions from salary.

- Example 2: Employers may match contributions.

IRA: No employer sponsorship.

- Example 1: You open it at a bank yourself.

- Example 2: Contributions are made directly by you.

3. Contribution Limits

403b: Higher annual contribution limits.

- Example 1: Employees can save a large portion of their salary.

- Example 2: Catch-up contributions allowed for long service.

IRA: Lower annual contribution limits.

- Example 1: Limited yearly cap.

- Example 2: Smaller catch-up option for age 50+.

4. Investment Options

403b: Limited to employer-selected plans.

- Example 1: Fixed annuities.

- Example 2: Mutual funds chosen by the employer.

IRA: Wide range of investments.

- Example 1: Stocks and bonds.

- Example 2: ETFs and mutual funds.

5. Tax Benefits

403b: Contributions are pre-tax (traditional option).

- Example 1: Lowers taxable income.

- Example 2: Taxes paid during withdrawal.

IRA: Can be traditional or Roth.

- Example 1: Traditional gives tax deduction.

- Example 2: Roth gives tax-free withdrawals.

6. Withdrawal Rules

403b: Penalty before age 59½ (with exceptions).

- Example 1: Early withdrawal penalty.

- Example 2: Loans may be allowed.

IRA: Similar age rule but no loan option.

- Example 1: Early penalty applies.

- Example 2: Certain hardship exceptions allowed.

7. Administrative Control

403b: Managed through employer’s provider.

- Example 1: Limited flexibility.

- Example 2: Changes require HR approval.

IRA: Fully controlled by account holder.

- Example 1: You choose the provider.

- Example 2: You manage investments independently.

8. Fees

403b: May include administrative fees.

- Example 1: Plan maintenance charges.

- Example 2: Annuity fees.

IRA: Depends on chosen broker.

- Example 1: Low-cost brokerage option.

- Example 2: Some accounts offer zero fees.

9. Portability

403b: Can be rolled over when changing jobs.

- Example 1: Transfer to IRA.

- Example 2: Move to another employer plan.

IRA: Remains with you regardless of job change.

- Example 1: No need to transfer.

- Example 2: Independent of employer.

10. Required Minimum Distributions (RMDs)

403b: RMDs required at a certain age (traditional).

- Example 1: Must withdraw after required age.

- Example 2: Penalty for not withdrawing.

IRA: RMDs apply to traditional, not Roth.

- Example 1: Traditional IRA requires RMD.

- Example 2: Roth IRA does not during owner’s lifetime.

Nature and Behaviour of Both

403b: Structured, employer-based, disciplined savings tool.

IRA: Flexible, independent, self-managed investment vehicle.

Why Are People Confused About Their Use?

People are confused because both are retirement plans with tax benefits. The names sound technical, and both involve long-term savings.

Their tax structures are similar, which makes the difference between 403b and IRA less obvious at first glance.

Table: Difference and Similarity Between 403b and IRA

| Feature | 403b | IRA | Similarity |

| Type | Employer-sponsored | Individually opened | Retirement account |

| Eligibility | Nonprofit/public employees | Anyone with income | Requires earned income |

| Contribution Limit | Higher | Lower | Annual limits apply |

| Tax Benefit | Pre-tax/Roth option | Traditional/Roth | Tax advantages |

| Portability | Transferable | Fully portable | Long-term savings |

Which Is Better in What Situation?

A 403b is better for employees of public schools or nonprofits who receive employer matching contributions.

Employer matching is free money and increases retirement savings quickly. It is suitable for disciplined payroll deductions and higher contribution limits.

An IRA is better for self-employed individuals or those who want investment flexibility. It is ideal for people who want control over their portfolio and lower fees.

Roth IRA is especially beneficial for young earners expecting higher future taxes.

Use in Metaphors and Similes

- “A 403b is like a company-sponsored safety net.”

- “An IRA is like planting your own financial garden.”

Connotative Meaning

403b: Neutral to positive (security, structure).

- Example: “Her 403b gave her peace of mind.”

IRA: Positive (independence, flexibility).

- Example: “His IRA symbolized financial freedom.”

Idioms or Proverbs Related

While no direct idioms exist for 403b or IRA, related financial idioms include:

- “Save for a rainy day.”

- Example: Opening an IRA helps you save for a rainy day.

- Example: Opening an IRA helps you save for a rainy day.

- “Don’t put all your eggs in one basket.”

- Example: Use both 403b and IRA to diversify savings.

- Example: Use both 403b and IRA to diversify savings.

Works in Literature (Mention of IRA)

- Atlas Shrugged – Novel, Ayn Rand, 1957 (Genre: Philosophical Fiction)

(Direct literary works specifically titled 403b are uncommon.)

Movies Related to Retirement or IRA Themes

- The Retirement Plan (2023, USA)

- About Schmidt (2002, USA)

(No major films specifically titled 403b.)

Five Frequently Asked Questions

1. Can I have both 403b and an IRA?

Yes, if eligible, you can contribute to both.

2. Is 403b better than IRA?

It depends on employer match and personal goals.

3. Can I roll over 403b into an IRA?

Yes, after leaving the job.

4. Which has higher contribution limits?

403b generally has higher limits.

5. Are both tax-advantaged?

Yes, both offer tax benefits.

How Both Are Useful for Surroundings

Both plans promote financial stability. When individuals save properly, society benefits from reduced economic dependency and increased investment growth.

Final Words for Both

403b provides structured and employer-supported retirement growth.

IRA offers independence and flexibility in investment decisions.

Conclusion

Understanding the difference between 403b and IRA is essential for smart retirement planning.

While both are tax-advantaged accounts designed to secure financial futures, their structure, eligibility, and flexibility vary significantly. A 403b works best for nonprofit and public employees seeking employer-supported savings.

An IRA suits individuals who want control and broader investment choices. By knowing their differences, individuals can build stronger retirement strategies, enhance financial literacy, and ensure long-term economic security.

I am Stephen King is a spiritual writer and digital creator dedicated to exploring the deeper meaning behind numbers, synchronicity, and divine guidance. Through his platform, spiritualdigits.com he shares insights on angel numbers, spiritual symbolism, and personal awakening to help readers align with their higher purpose. His work blends intuition, research, and practical wisdom to make spiritual concepts clear, accessible, and transformative.